Niger’s soaring bad loans cast shadow over uemoa’s financial stability

The January 2026 economic outlook report delivers a stark verdict: while the banking sector of the West African Economic and Monetary Union (WAEMU) achieves symbolic milestones, it grapples with a mounting tide of risks. At the epicenter of this turmoil, Niger stands out with an unprecedented non-performing loan ratio, epitomizing a deepening regional divide.

The Niger Factor: A Disturbing Peak in Asset Degradation

As the Union strives to shore up its financial system, Niger’s performance remains the most troubling across the bloc. Despite marginal improvements, the country continues to lag far behind as the most vulnerable link in the regional banking network.

A Troubling Leader in the Rankings

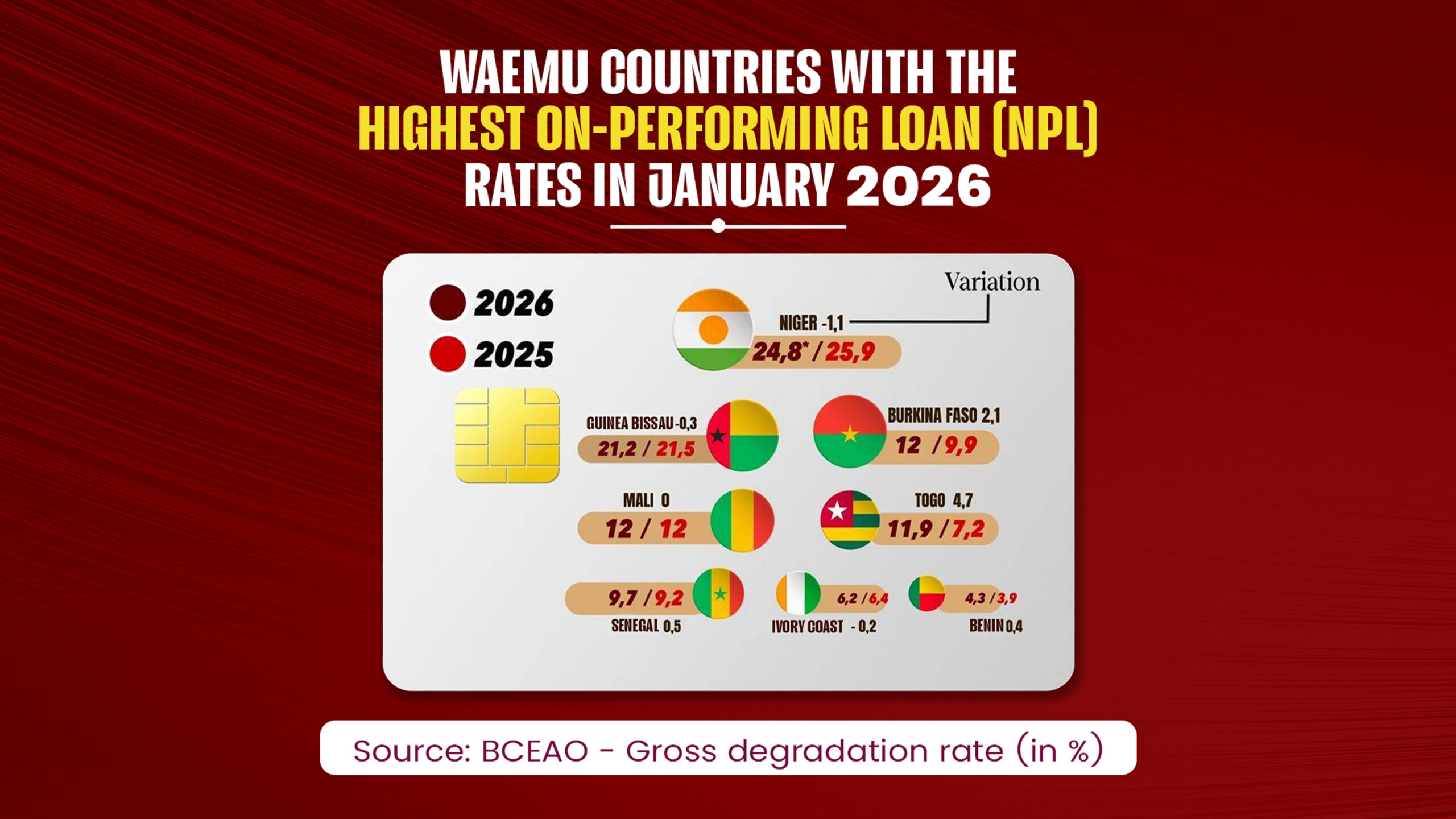

With a staggering 24.8% non-performing loan rate in January 2026, Niger holds the unenviable title of the worst performer in the Union. Nearly one in four loans disbursed in the country is now in default—a figure that, while slightly improved from 25.9% in 2025, highlights a structural vulnerability exacerbated by security tensions and political instability.

A Two-Speed Union: The Sahelian Divide

The January 2026 data underscores a sharp divide between coastal economies and the Sahelian bloc, where Niger serves as the crisis’s focal point.

The Sahelian Bloc Under Severe Strain

Beyond Niger, Sahelian nations are also grappling with alarming deterioration:

- Mali and Burkina Faso: Both nations register a 12% non-performing loan rate, with Burkina Faso experiencing a sharp rise of 2.1 percentage points over the past year.

- Guinea-Bissau: The country remains mired in critical territory with a 21.2% default rate.

Coastal Resilience: A Relative Bright Spot

In contrast, coastal economies exhibit greater resilience, though not without concerns:

- Benin: Leading the Union with the lowest default rate at 4.3%.

- Ivory Coast & Senegal: Both maintain relative stability with rates of 6.2% and 9.7%, respectively.

- Togo’s Anomaly: The country defies the trend with a dramatic surge in defaults, jumping from 7.2% to 11.9% (+4.7 percentage points).

The Big Picture: Credit Growth Overshadowed by Caution

The total loan portfolio has surpassed the historic threshold of 40.031 trillion FCFA (+4.7% year-on-year), yet the momentum appears stifled by growing unease.

A Warning Signal: Soaring Bad Loans

Non-performing loans have ballooned to 3.631 trillion FCFA, while the coverage ratio has plummeted to 59%. This suggests banks are struggling to provision for losses at the same pace as defaults escalate.

Why the Slowdown?

The deteriorating risk profile of countries like Niger has forced banks to rethink their strategies:

- Stricter Lending Terms: Increased personal contributions and tougher collateral requirements.

- Heightened Selectivity: Banks now prioritize balance sheet security over credit expansion, risking a slowdown in financing for local SMEs and SMEs.

As 2026 begins, the WAEMU banking system stands at a crossroads. While systemic collapse remains unlikely, Niger’s struggles and the ripple effect across the Sahel demand unwavering vigilance to avert a potential liquidity crisis.